Research-Driven.

A complex and ever-changing investment landscape provides challenge and purpose for our team.

Long Short Equity – Brighter Days Ahead?

January, 2024 | Alex Moore

Long Short Equity – Brighter Days Ahead?

In Las Vegas casinos, one of the oldest and rowdiest games is craps. Craps is a dice game where players bet on the outcomes from a roll of two dice thrown by a “shooter.” One of the reasons that gamblers gravitate towards craps is because there are close to 60 different bets that a player can make. These different bets have a wide range of odds (i.e., probability of occurring) and payouts associated with them. Of all the different bets in craps, the Any Seven bet is perhaps the most popular and well-known wager. When a gambler bets Any Seven, they are betting that the shooter will roll a 7 on the next roll. The number 7 is the most frequent and probable number to appear when the dice are rolled because the odds of rolling a 7 are 6 in 36 or 5:1 odds against the better. The house (i.e., casino) only pays out 4:1 on a winning Any Seven bet, which makes this the absolute worst bet you can make in craps. In fact, the Any Seven bet is one of the worst risk-adjusted bets a gambler can make in any casino game because of the disparity between the odds and the payout ratio.

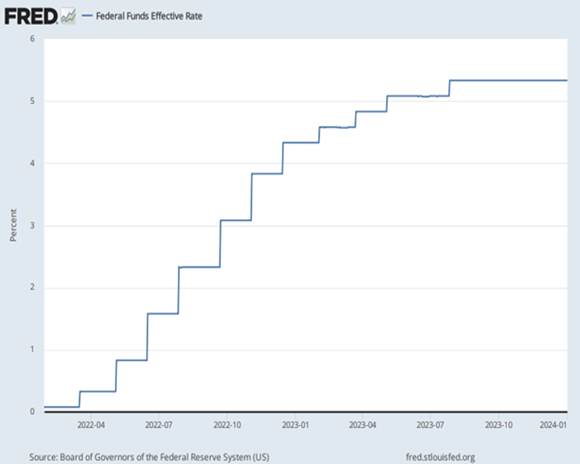

Going into 2023, investing with the expectation that the S&P 500 and MSCI World Indexes would be up over 20% for the year certainly would have seemed like gambling (more on this point later). The Federal Reserve was raising interest rates at the fastest pace since the 1980s. The consensus market forecast implied a 66% probability that the U.S. economy was headed for a recession. Wall Street expected earnings growth for the S&P 500 Index to be flat to negative based on the anticipated recession. The S&P 500 Index’s forward price-to-earnings ratio was 17, which is not cheap from a historical perspective.

As telegraphed by Federal Reserve Chair Powell, the Fed did raise rates four times in 2023, making a total of 11 hikes since the start of the tightening cycle. In March, the cumulative impact of higher rates caused enough mark-to-market damage to the balance sheets of several high-profile regional banks (e.g., Silicon Valley Bank, Signature, First Republic) that the FDIC liquidated them. In addition, geopolitical risks materially increased over the course of the year as the war in Ukraine continued and another regional war broke out in the Middle East when Hamas, a terrorist organization, attacked Israel. Typically, any one of these events, in isolation, would be enough to derail equity markets.

In the end, all that mattered was that inflation rapidly declined towards the Fed’s 2% target, there was no recession, and seven stocks, known as the Magnificent Seven (Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla, and Meta), propelled the market higher. Investors’ hopes that these seven companies would generate windfall profits from Artificial Intelligence pushed their collective prices up 86.7% for the year.1 The December 17th headline article in the Wall Street Journal declared, “It’s the Magnificent Seven’s Market. The Other Stocks Are Just Living in It.” There is no hyperbole in that statement when you look at the attribution data. The Magnificent Seven contributed 10.6 points of the MSCI World Index’s 24.4% return for 2023, an amazing 43.3%. The MSCI World Index has 1,480 stocks that cover approximately 85% of the free float-adjusted market capitalization in each country. The total market capitalization of the Magnificent Seven is now greater than the combined equity markets of the United Kingdom, Canada, and Japan. The story was similar when you look at how these seven stocks performed relative to the other 493 stocks in the S&P 500 Index. Currently, the Magnificent Seven make up roughly 28% of the S&P 500 Index’s total market capitalization. This level of concentration is unprecedented in the index’s history.

Admittedly, the S&P 500 and the MSCI World Indexes both had good years, even if you exclude the performance of the Magnificent Seven. The point of disaggregating the return of the indexes is to highlight the level of concentration risk that an investor had to take to achieve this result in 2023. As a fiduciary, there is no way that the portfolio management team would ever construct a long/short equity portfolio with this level of concentration risk. The risk emanates from the extraordinary weighting of just seven stocks, and the fact that all seven companies reside in the technology sector. To be clear, the team understands that the Magnificent Seven are very good companies with high growth rates, strong balance sheets, and are well positioned to take advantage of Artificial Intelligence. Many active managers certainly have exposure to these companies, just not anywhere near the same level of concentration as the index. In our final analysis, the benchmark’s performance for 2023 seems more like an Any Seven craps bet that hit versus a prudent investment strategy.

Recently, the investment team made its traditional January research trip to New York City to meet with several of our long/short equity managers. The trip is a great opportunity to review the previous year with our managers and to get their perspective on industry dynamics. One of the biggest takeaways from these meetings is that fundamental long/short equity, as a strategy, is still very much out of favor. You can see this trend across different data sets. One manager commented,

“50% [of the float] shorted used to be high, now it’s like 25% on heavily shorted names. People don’t short [stocks] anymore …. Our track record is very good and nobody seems to care. I don’t see any of my peers in the space raising money either. The data is squishy and hard to aggregate, but my take is that the hedge fund industry has grown a lot in the past decade and AUM for fundamental long/short is the same, maybe a little less. As a percentage it has declined a lot.”

This perspective was the consensus across all our meetings. In addition, the “less competition theme” is consistent with our observations on industry allocation trends. Less competition in combination with other structural tailwinds that we have discussed previously, like increasing stock dispersion and price volatility, make long/short equity a compelling contrarian bet in our opinion – certainly much better than an index or Any Seven bet.

January 2024

Alex Moore

1The Magnificent Seven stocks were up 105% for 2023 utilizing a simple price average versus the capitalization weighted average which is quoted.